|

ROBERT F. MULLIGAN

|

|

A Brief Introduction to

Econometrics

1.

The basic univariate model: Yt = a + bXt + et.

Y is called the left-hand-side variable, LHS variable, the dependent variable, or

the explained variable. X is the right-hand-side, RHS variable, dependent, or

explanatory variable. e is the residual, error, or disturbance term. The

expression (a + bXt) is called the fitted value of Y and is also

referred to as Y-hat. The regression calculates values of a and b, the

"regression coefficients," that best fit the data for X and Y (hence

regression is sometimes called "curve fitting,") by minimizing the

sum of squared residuals, ∑tet2 (or e'e

in vector notation.) This most basic and

commonly used regression technique is called ordinary least squares, OLS, OLSQ,

or LS.

To run a

regression in MS Excel 97, enter your data in a worksheet. Normally each

variable is placed in its own column, with the name of the variable and any

other information you may wish to place there, like units and data

transformations you performed (which are not used for computing the regression

coefficients), at the top of the column. Click on "Tools" in

the toolbar at the top of the screen to get the "Tools" menu, then go

down to the bottom and click on "Data Analysis." Scroll down

the "Data Analysis" window until you find "Regression,"

highlight it, and press "enter." You will be provided a dialog

box which enables you to set the range for each variable in the regression.

Y is the left-hand-side variable. Click on the Icon on the right side of

the window for the Y variable range (it looks like a little table with tiny

text windows - real cute.) Then highlight all the numerical values of the

LHS variable. The screen will show a dotted line around the numbers you

highlight. Press enter, and the dialog box will reappear with the range

of the LHS variable you selected. Repeat for the RHS variable. You

can highlight more than one column on the RHS to estimate a multivariate

regression. Make sure each variable has the same number of

observations. When you are satisfied with the Y and X ranges in the

dialog box, click on the "OK" button, and your output will appear on

a new sheet in your current worksheet.

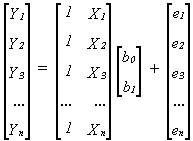

2. The

basic univariate model in vector notation: y = Xβ + e where y is an (n x 1)

column vector of the different observations of the left-hand-side variable, X

is an (n x 2) matrix for which the first column is a column of ones

(representing the constant or intercept term) and the second column is a column

of the n observations of the right-hand-side variable, β is a (2 x 1) vector of estimated

coefficients (the intercept or constant, and the slope or X coefficient,) and e

is an (n x 1) vector of residuals or disturbance terms. This model is the same

as in part 1, and looks like this:

|

|

Note

that I have renamed the intercept b0 (instead of a) and the slope b1

(instead of just b).

In

MS Excel 97, you can force the regression line through the origin, setting a =

b0 = 0, by checking the "Constant is Zero" option

on the regression dialog box.

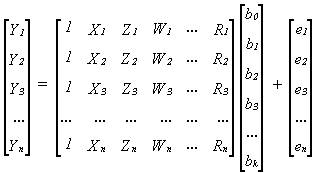

3.

The basic multivariate model (in vector notation): y = Xβ + e is the same as the simple univariate

case except that now X is an (n x k+1) matrix (called the observation or

data or independent variable matrix) consisting of a column of n ones

(representing the intercept) and k columns of n observations of the k

right-hand-side variables, and β is a (k+1 x 1)

column vector of estimated coefficients. This model has more than just one

explanatory or independent variable and looks like this:

|

|

This

model can also be written as: Yt = b0 + b1Xt

+ b2Zt + b3Wt + b4Rt

+ et, supposing there are only four right-hand-side variables.

In

MS Excel 97, you estimate a multivariate regression by selecting an X range

with more than one column, which the software reads as more than one

variable. It is important each column has the same height, lined up row

by row, and that each column be adjacent.

4.

Non-linear regression: What if Y is a function of X, but not a linear

function of X? Then form second-order terms by squaring each X, and estimate

the regression as: Yt = a + bXt + cXt2

+ et. You can also cube X or raise it to any power you want. If it

is a multivariate regression, (with, say, X and Z as right-hand-side

variables,) you can also add cross-product terms (in this case XZ as well as X2

and Z2.)

You

could do this by creating new columns from your original X variables. Or

you could transform your data into logarithms.

5.

Some regression output:

MS Excel

97 provides three output tables whenever you run a regression.

Excel

Table 1: Regression Statistics

The first table gives statistics which measure the fit of the regression as a

whole. The multiple R is the coefficient of correlation between Y and

Y-hat. (For a univariate regression, with only one RHS variable, R is the

coefficient of correlation between X and Y). R is the square root of the R-squared, the

coefficient of determination. The range of R is between -1 and +1, so

R-squared ranges from 0 to 1. Theoretically, the adjusted R-squared, the

coefficient of determination adjusted for degrees of freedom, or R-bar-squared,

has the same range, but it can be negative when the number of coefficients

being estimated—that is, the number of RHS variables—is high compared to the

number of observations or sample size. R-squared = R-bar-squared = 1

indicate a perfect fit. The closer these are to one, the better the

regression fits the data. The standard error of the regression, which

should be as low as possible, and the number of observation are also provided.

Excel

Table 2: The F-Statistic

The second table, labeled ANOVA for "Analysis of Variance," computes

an F statistic which tests whether the estimated coefficients (the b's) are

jointly significantly different from zero. The last column in this table

gives the significance level of the F test, which should be less than or equal

to 5% (= 0.05) or some other arbitrarily chosen low percentage. The

table gives degrees of freedom ("df") and sums of squares

("SS") for the regression (SSR), the residuals or error terms (SSE),

and the total, for the LHS variable (SST). To get the SST, square each

observation of the LHS variable and add the squares. To get the SSE,

square each error term and add the squares. To get the SSR, subtract SSE

from SST, or square each value of Y-hat (the fitted values of Y) and add the

squares.

Next,

the table gives mean squares, which are the SSR and SSE divided by their

degrees of freedom. For the SSR, the df is the number of RHS variables

with coefficients being estimated, not including the constant. The

df for the SSE is the number of observations, minus the number of coefficients

being estimated, including the constant. The SSR and SSE df add up

to one less than the number of observations (1 - n), which is the SST df.

One degree of freedom is eaten up by the constant, which is why the SST df is

one less than the number of observations of each variable, as long as a

constant is included in the regression.

The

ratio of the two mean squares MSR/MSE is F-distributed under ideal

conditions. This is listed under F. MST is not used to calculate

the F statistic, so it is not listed in the ANOVA table. The F ratio

tests the joint hypothesis H0: (b1 = b2 = b3

= . . . = bk = 0), the null hypothesis that all the b

coefficients (except b0 the intercept or constant) are

jointly equal to zero. The significance level of the F ratio is greater than 5%

(or some other low value you choose) to accept (or "fail to

reject") the null hypothesis, which tells you the regression has no

explanatory power. The significance level of the F ratio is less than 5% (or

some other value you choose) to reject the null hypothesis, which tells you the

regression has some explanatory power.

Excel

Table 3: Estimated Coefficients and their t-Statistics

The third table provides (finally!) the estimated coefficients for the intercept

and each RHS X variable. Each coefficient has a standard error. The

t-statistic or t-ratio is the ratio of each coefficient divided by its standard

error. Each t-ratio is t-distributed under ideal conditions. Each t

test tests the null hypothesis H0: (bj = 0), that

each coefficient is equal to zero. The t-statistic independently tests

the significance of each estimated coefficient while the F jointly tests

whether they all work together. Usually

if any t-stats are greater than 2.00, the F statistic will also be

significant. The significance level of

the t ratio is greater than 5% (or some other low value you choose) to

accept (or "fail to reject") the null hypothesis, which tells you the

variable may be removed from the regression, so take it out and estimate the

regression without it. The significance level of the t ratio is less than 5%

(or some other value you choose) to reject the null hypothesis, which tells you

the variable may be kept.

In

addition to estimated coefficients for each variable and the intercept or

constant term, most regression softwares provide some or all of the following:

1.

Standard error (of a coefficient) tells you how likely the true or population

value of the estimated coefficient will lie within a certain distance from the

estimate (or sample value,) based on the dispersion of the data. The smaller

the better. The true value is about 67% likely to lie within plus or minus one

standard error from the estimated value, and about 95% likely to lie within

plus or minus two standard errors. MS Excel 97 provides this in the

coefficient estimate table.

2.

t-statistic (t-ratio): The estimated coefficient divided by its standard error.

The higher the better. If t exceeds 1, it is at least about 67% likely that the

true value of the coefficient is not zero, and if t exceeds 2, it is at least

about 95% likely. This tests the hypothesis that the true value of an estimated

coefficient is equal to zero, and that that variable should be deleted.

MS Excel 97 provides this next to the standard error in the coefficient

estimate table.

3.

Probability value of the t statistic (2-tailed significance level): Gives the

probability value of the computed t statistic from an internal table of the t

distribution. The lower the better. Less than .05 (or .10 or .01, this is

called an alpha or level of significance, which you choose) for statistically

significant coefficients.

4. R2

(Coefficient of determination): Ranges from 0 to 1. The higher the better.

Measures the % of variation in Y that is explained by variation in the

right-hand-side variables. In a univariate regression it is the square of the

coefficient of correlation (rXY) between X and Y. It is calculated

by this formula:

|

|

Y-bar is

the sample mean of Y, SSE means "sum of squared errors" (or sum of

squared residuals, e'e in vector

notation), and SST means "sum of squares total." SSR is the "sum

of squares regression," and they all fit into this identity: SST = SSR +

SSE. SSE can't be referred to as SSR (though, unfortunately, sometimes it is.)

To make things more confusing, SSR is also called the "explained sum of

squares" because it's what's explained by the regression, and SSE is also

known as the "unexplained sum of squares," because it's what's left

over. If the regression were a perfect fit, all the e's would be zero, and so

SSE would equal zero and R2 would equal one. (This would mean that

SSR = SST.) MS Excel 97 provides the R2 in the regression

statistics table, just under its square root, "Multiple R."

5.

Adjusted R2 (R2 adjusted for degrees of freedom, aka

R-bar-squared): Interpreted the same way as R2, but can be negative.

Should never be greater than R2. It is calculated by this formula:

|

|

The

formula is basically the same as for R2, but includes adjustments

for the size of the sample (n) and the number of coefficients being estimated

(k+1). MS Excel 97 provides this in the regression statistics table under

the R2.

6.

Durbin-Watson statistic (DW or d): Tests for serial correlation of residuals:

Serial correlation means that the error terms are systematically related

through time, and not statistically independent of each other. Theoretically

the errors should be white noise, or perfectly random. When they aren't, the

whole estimate's validity is questionable. DW is close to 2 in the absence of

serial correlation. Critical values for DW can be found in the (old)

Durbin-Watson or (newer) Savin-White tables in the back of most econometrics

texts. In cross-sectional data, serial correlation is called autocorrelation,

and can be solved by just scrambling the order of the data (basically you can

do this because the order of the observations wasn't important to start with.)

With time-series data—commonly used in macroeconomics—you can't change the

order, so you have two choices: difference your regression equation (see

below), or apply a correction for serial correlation of the error terms,

typically the Cochrane-Orcutt iterative correction (provided by MicroTSP) or

Beach-MacKinnon iterative maximum likelihood method (provided by TSP). MS

Excel 97 does not provide a test for serial correlation or an estimation

technique robust to serial correlation.

7.

Durbin's h and/or Durbin's h alternative: TSP provides this, but MicroTSP

doesn't (yet). It's an improved test statistic for serial correlation and should

be used in preference to DW whenever there are a large number of explanatory

variables, or when some of the explanatory variables are lagged values of Y.

TSP 4.2 prints out the probability, which you want to be less than the

significance level you choose, a = .10, .05, or .01. MS Excel 97 does not

provide a test for serial correlation. Too bad.

8. Log

likelihood (logarithm of the likelihood function): If n is the number of

observations of each variable in the regression, this is calculated by the formula:

|

|

The

larger L the better (consequently the larger logL the better) but this is only

meaningful when comparing two regressions: the one with the larger logL is the

better of the two. The difference of the logL's is chi-square distributed, and if

its probability value is below some critical significance level (a), usually

.05, the model with the lower likelihood is rejected. This is called a

likelihood ratio test because the test statistic (the difference between

logL's) is the log of a ratio. The formula used for the log likelihood is based

on the normal distribution; theoretically the distribution of the residuals

should become more nearly normal as the number of observations n approaches

infinity. Maximum likelihood estimation is an alternative technique to least

squares that chooses the estimated coefficients to make the residuals most

nearly normally distributed. Instead of minimizing the sum of squared

residuals, it maximizes the value of the normal likelihood function. The higher

logL is for a least squares estimate, the closer it is to the maximum

likelihood or ML estimate. It is not always useful to assume that residuals are

normally distributed, see sect. 7.5 below. MS Excel 97 does not provide

this.

9.

Standard error of the regression: Measures the magnitude of the residuals.

About 67% will lie between one standard error above zero and one below, and

about 95% will lie between plus or minus two standard errors. The smaller the

better. MS Excel 97 provides this in the first regression output table,

under "Standard Error."

10. Sum

of squared residuals: (e'e) This is what is minimized by a least squares

estimate. The smaller the better. MS Excel 97 provides this in the SS

column of the ANOVA table, under "Residual."

11. F

statistic (zero slopes): Tests whether the estimated values of the coefficients

are all significantly different from zero. Doesn't include the constant or

intercept. For a univariate regression is equal to the square of the t

statistic for the right-hand-side variable. The higher the better. You want the

probability value of the F statistic to be less than a = .10, .05, or .01. MS

Excel 97 provides the F statistic and its probability level at the far right of

the ANOVA table.

12.

Akaike Information Criterion (AIC): AIC

= ln(SSE/n) + 2k/n, where n is the number of observations or sample size, k is

the number of coefficients being estimated, including the constant if any, and

SSE is the sum of squared residuals from the regression, aka e'e.

The lower this number is, the more efficient the regression model is in

making use of the available information contained in the data to estimate the

regression coefficients. Note that the

formulas for the three information criteria are similar to the R-square.

R-square always increases when additional RHS variables are added. The information criteria attempt to measure

whether the information contained in additional RHS variables, which always

increases the R-square, is sufficient to warrant adding more variables to the

model. If adding a variable to the

regression results in the AIC falling, then add the variable. If removing a variable results in the AIC

falling, then remove the variable. The

AIC is automatically computed by Eviews, but not by MS Excel.

13. Schwarz Bayesian Information Criterion (SBIC

or SC): SBIC = ln(SSE/n) + (k

ln(n))/n. The SBIC is an alternative

approach to measuring the information efficiency of a regression model. SBIC is interpreted the same as the other

information criteria, but does not always give the same results. It is automatically computed by Eviews as

part of the regression output, but not by MS Excel.

14. Amemiya's Prediction Criterion (PC): Amemiya's PC = SSE(1 + k/n)/(n – k). Amemiya's PC is yet another approach to

measuring the information efficiency of a regression model. This is interpreted the same way as the AIC

or the SBIC, lower is better, but does not always give the same results. It is not computed by either Eviews or MS

Excel.

5.

The kinds of data.

a.

Time-series data: A different value of each variable is observed for each

period of time, e.g., annually, quarterly, monthly, weekly, daily, etc. Gross

domestic product (GDP), interest rates, stock market quotations are examples.

Used mostly by macroeconomists, and is often subject to serial

correlation. ECON 300 Forecasting Projects will deal mostly with

time-series data.

b.

Cross-sectional data: Each observation of each variable is for a different unit

being observed, e.g., different firms, plants, households, individuals. Census

data on the number of lathe machines operated at different factories, the

number of workers employed by different firms, the size of different households

are examples. Used mostly by microeconomists, and the order can be scrambled if

it improves regression estimates.

c. Panel

data: Each observation is for a specific unit and a specific point in time. A

set of time series consisting of the number of workers employed by different

firms over several years would be panel data. Used mostly by microeconomists.

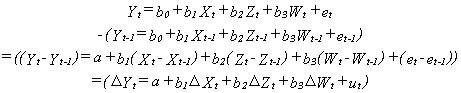

6.

Differencing a regression: If a time-series regression has serial correlated

residuals, or if any one of the variables is non-stationary, that is, if a

variable has a moving trend like GDP, CPI, or many other steadily-growing

macroeconomic variables, or has a cyclical pattern of variation, the regression

can be differenced. This involves lagging the equation one time period, then

taking the difference:

|

|

The b0

drops out, but all the other b's (the slopes) retain their identities, so this

is an alternative way of estimating the slopes. The equation can be differenced

as many times as necessary to achieve acceptable Durbin-Watson or Durbin's h

statistics. An intercept term (I call it "a") is left in the

differenced equation, even though it doesn't belong there. This is because if

you estimate the regression without an intercept, that imposes the very

unrealistic restriction that the regression line passes through the origin. It

is better to estimate the unrestricted equation, though a is not the same as b0.

Also the u's are different from the (serial correlated) e's.

Undifferenced

regressions with non-stationary data can benefit from the desirable statistical

property of superconsistency. This

means that the estimated coefficients converge to their true, unbiased values

faster than for OLS estimates with stationary data. Superconsistency is a large sample property,

and the dividing line between large and small samples is ambiguous. A sample less than 30 observations is always

"small," but a sample less than 300 observations may not be

"large."

7.

Violations of regression assumptions:

1.

Heteroskedasticity: Regression theory assumes homoskedasticity of regression

residuals, that is, that the residuals have a constant variance, (otherwise the

standard error of the regression would vary systematically.) If you have this,

invoke White's heteroskedasticity consistent covariance matrix to compute the

results. In MicroTSP use the command [LS(H) Y C X Z W] in TSP use [OLSQ

(ROBUST) Y C,X,Z,W ;]. How do you know if you have it? If you don't get the

same answer without White's matrix as with it, heteroskedasticity is the reason

why. There are a battery of statistical hypothesis tests available to test for

heteroskedasticity, but it's much easier to estimate the regression both

ways. MS Excel 97 does not provide this.

2.

Serial correlation (or Autocorrelation): Use the Cochrane-Orcutt correction in

MicroTSP: [LS Y C X Z W AR(1)]. If necessary, add AR(2) or more terms as well.

When the Durbin-Watson statistic goes close to two, this problem is solved. You

can also difference the equation, see section 6. In TSP use the Beach-MacKinnon

iterative maximum likelihood technique: [AR1 Y C,X,Z,W ;], but usually this

only works for annual data because you can't add more terms if you need to.

With cross-sectional data, just change the order of the data, (you can do this

as long as the order doesn't matter.) MS Excel 97 does not provide this.

3.

Multicollinearity (1): Some of your variables are too similar for the computer

algorithm for minimizing the sum of squared residuals (e'e) to handle.

You'll get an error message regarding a "near singular matrix" which

the computer can't invert (see section 8 below). Excel returns the LINEST

function. There are two possibilities:

a. It is

an exactly singular matrix (the computer can't tell the difference)

because you have accidentally entered the same variable twice in the same

regression. Look for the left-hand-side variable on the right, or one of the

right-hand-side variables repeated. Excel's LINEST function error message

indicates the regression cannot be computed because one variable is a linear

function of another. One of the few advantages of MS Excel 97 is that Excel

is so user-hostile it is very difficult to make this mistake.

b. One

(or more) of your variables is very much smaller in relative magnitude than the

rest. This is called a scale problem. The computer treats it as a string of

zeroes, and it's a linear function of the string of ones it uses for the

constant. You can tell if you have this by plotting all your data together: in

MicroTSP the command is: [PLOT Y X Z W]. In MS Excel 97, plot your data by

clicking on the "chart wizard" icon on the standard toolbar. It

looks like a bar chart. If one variable is just about always equal to

zero on the plot, then you should select some time period and divide each

variable by its own value for that time period. This is called indexing, and

should remove any scale problems.

4.

Multicollinearity (2): Although the software can successfully perform the

estimate, it is difficult to interpret. (This is a less serious problem.)

Typically you may find that the F statistic is very high (indicating a good

estimate and a good model,) but the t statistics are all very low, (indicating

that many or all of the variables should be removed from the model.) It is O.K.

to remove variables from the model as long as the F statistic remains high (or

its probability level remains low.) If you cannot remove any variables

without hurting your F statistic, just note multicollinearity as the reason why

the t statistics are so low.

5.

Non-normality: Contrary to common opinion, it is not a requirement of the

standard regression model that regression residuals be normally distributed.

However, if they are normally distributed, that guarantees that the residuals

are also homoskedastic and not serially correlated. To test for normality,

calculate the Jarque-Bera efficient normality test statistic. In MicroTSP,

right after you run the regression, use: [HIST RESID] and the Jarque-Bera

statistic will be at the bottom of the histogram, next to its probability

level. J-B tests the null hypothesis of normality. You want the probability to

be greater (not less) than .05, or some other significance level,

otherwise the residuals aren't normally distributed. TSP does this

automatically whenever you estimate a least squares regression, but in MicroTSP

you can test any variable for normality with the HIST command, which is very

convenient. SAS does a different test, the Wilson statistic, with the PROC

UNIVARIATE command. The closer the Wilson statistic is to one, the more nearly

normal the variable being tested. The traditional test for normality, the

Kolmolgorov-Smirnoff test, was difficult to compute, and was invented by two

Russian mathematicians. The Jarque-Bera test was invented by economists. If

your residuals are normally distributed, you can claim that your estimate is

close to the maximum likelihood estimate.

MS Excel

97 does not provide a test for normality, but you can compute skewness and

kurtosis of your residuals with the "Descriptive Statistics" option

in the "Data Analysis" menu. The skewness of the normal

distribution is 0 and the kurtosis 3. Check the "Residuals" box in

the regression dialog box to save your residuals when you run a regression.

8.

Regression computations: (Inverting the matrix). In the general multivariate

regression model, y = Xβ + e, a

least squares regression is performed by calculating an estimate of β, called b. Both b and β are (k+1 x 1) column vectors. The least

squares formula is b = (X'X)-1X'y. The matrix

formulae X'X and X'y are not too difficult to calculate, even

with large numbers of explanatory variables. However, inverting the matrix X'X

to get (X'X)-1 is not easy, and before the days of computers

(up until the early sixties), regressions could not generally be calculated

with more than five or six right-hand-side variables. Even supercomputers have

been known to balk at large inversion problems.

9.

Some alternatives to ordinary least squares: (none are provided by MS Excel

97)

1.

Single equation techniques:

a.

minimum absolute deviation (MAD)

b.

minimum sum of absolute errors (MSAE)

c.

instrumental variables (IV) [You can do this in MS Excel 97, but you have to do

all the work yourself.]

d.

two-stage least squares (2SLS) [This can be done in Excel the same as with

instrumental variables.]

e.

weighted least squares

f.

limited information maximum likelihood (LIML)

g.

full information maximum likelihood (FIML or just ML)

h.

recursive least squares

i.

Kalman filtering

j.

non-linear least squares (NLS)

k.

least median of squares (LMS) [This is an outlier-resistant technique designed

to avoid having the estimate unduly influenced by unusually large or small

observations.]

2.

Simultaneous equation techniques

a.

seemingly unrelated regressions (Zellner's method) (SUR)

b.

limited information maximum likelihood (LIML)

c.

full information maximum likelihood (FIML or just ML)

d.

three stage least squares (3SLS)

e.

generalized method of moments (GMM)