Based on the Quantity Theory

JACK METCALF and JASON SPAINHOUR

College of Business

Western Carolina University

Abstract

Over

the next two years, the level of the nations M1 money supply is forecasted

to have minimal volatility.This

forecast is based on the Monetarist Theory, assuming that the M1 money

supply is influenced greatly by the monetary base and money multiplier.The

forecast uses two-year-lagged long-term interest rates and variable real

GDP measured in chained 1996 dollars, adjusted annual rates, and seasonally

adjusted money stock from prior quarters.The

U.S. economy is currently operating in a period of low inflation while

growing tremendously. The ideal economic environment, has been closely

monitored by the Federal Reserve.The

Feds responsibility lies in its ability to keep inflationary pressures

from causing consumer prices to skyrocket.One

such way the Federal Reserve is able to fight inflation is through monetary

policy combined with either raising or lowering interest rates.The

most effective way in which the Federal Reserve is able to impose the corrective

measures necessary is through the use of accurate forecasts.Forecasts

are necessary since there is a time lag involved between the time monetary

and interest rate changes are issued and the period upon these measures

will effect.Interest rate data

from the period January 1995 through December 1999 was used to forecast

was used to forecastintereto either

help spur economic growth or induce a slow down gives The Federal Reserve

will pull

Part 1.

Introduction

This

paper forecasts the U.S. Money Supply quantity for the years 2000 and 2001.The

explanatory variable in our model is real GDP chained in 1996 dollars (GDPC

96) for the years 2000 and 2001.The

approach is based on the Monetarist model using the Quantum Theory: the

variables are the Federal Funds rate (FEDFUNDSR) and the seasonally adjusted

money supply (M1SL) which are both lagged by eight periods.The

Monetarist Theorem helps forecast economic peaks and troughs related to

inflationary and recession periods.The

amount of GDP is a dependent variable with the quantity of the money supply.

According

to our data obtained from the Federal Reserve Bank of St Louis, the M1

money supply is forecasted to have low volatility during the forecasted

period of 2000 - 2001.The forecast

horizon of two years lowers the risk of an inaccurate forecast. Due to

the complex variables involved, a large margin of error is present in any

forecast dealing with the money supply.The

forecast horizon is short enough to avoid seriously overstating or understating

the transactional velocity of the money supply.

The

rest of the paper is organized as follows: Part 2. Presents the data used

to forecast the money supply; Part 3. Presents the theoretical basis for

the approach adopted in forecasting the money supply; Part 4. Presents

forecasts of money supply for 2000 and 2001; Part 5. Evaluates the importance

of the forecast for the economy; and Part 6. Discusses conclusions for

economic policy.

Part 2.

Data

All

variables are taken from the Federal Reserve Bank of St Louis Federal Reserve

Economic Data (FRED). The measures of M1 money supply, gross domestic product,

and interest rates are FRED variables M1SL, GDPC96, and FEDFUNDS, and are

all quarterly adjusted nominal rates.The

variable GDPC96 was listed quarterly while the data for M1SL and FEDFUNDS

were both given by monthly variation.The

seasonally adjusted nominal variable M1 and Federal Funds rate were converted

to a real variable by averaging the three month period which comprised

the four annual quarters. This sample data includes the variables contained

within the period of 1993-99.The

forecast horizon is two years (eight quarters) into the future. Regression

analysis was first done on the original data to establish that a relationship

exists between the variables.

Part 3.The

Monetarist Variables Effect on M1 Money Supply

The long run level or change in the M1 supply is largely determined by the level or change in the monetary base along with the currency ratio.However, on a short term basis the M1 supply is influenced by economic variables such as interest rates, income, and wealth.

Part 4.

The Money Supply: A Short but Accurate Projection Through 2001

The

equation used to estimate M1 money supply for the years 2000 and 2001 were

done by a regression formula for the years 1993-1999. The data input was

the Federal Funds Rate, GDP, and the M1 money supply lagged eight periods

for these years. The R-squared of the estimate is 0.919. This indicates

that approximately 92% of the variations in the Federal Funds Rate and

GDP are explained by the lagged M1.The

t-statistic is less than one, indicating a slight rejection of the null

hypothesis. The t-statistic of the intercept is greater than ten, indicating

a strong rejection of the null hypothesis that the intercept equals zero.The

F-statistic for the hypothesis is 60.89.

M1SL

=(1369.937)-(.20148)( 1068.47)M1t-8+(.008518)(8277.27)Yt-8-(23.245)(5.52)It-8

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coefficients

|

|

|

Intercept

|

1369.94

|

10.63

|

|

X Variable 1

|

-0.201

|

-2.76

|

|

X Variable 2

|

0.00852

|

0.857

|

|

X Variable 3

|

-23.25

|

-6.48

|

Forecast

for M1 from the regression estimate is presented in Table 1.

Table 1

1999.1

2000.4 (billions of 1993-1999 dollars) |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This

represents a minimal variation in the amount of M1 available to consumers

with two explanatory variables, Being the Federal Funds Rate and GDP. These

are reasonable projections as long as the unemployment rate continues to

decline and there are no real changes in wages or inflation.

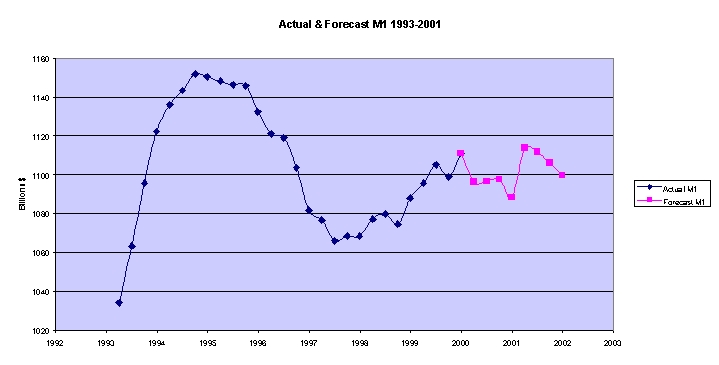

The

following chart illustrates our predictions:

Figure

1

The chart illustrates that throughout the year 2000 the M1 money supply will decrease which may coincide with the Federal Reserves increase of the Federal Funds and Discount Rate.Our prediction may be valid according to the Federal Reserves economic policy.In 2001, our prediction shows a huge increase in the first quarter and then a correction in the last three quarters of the year.Interest rates will affect the overall quantity of the money, which is determined by the Federal Reserve.

Part 5.

Forecast Implications: Steady as She Goes

The

M1 money supply is important to forecast because it indicates the amount

of money in circulation. The forecast of increasing and decreasing M1 indicates

economic activity will grow steadily in the future bearing mild corrections

in the market. There will be a constant argument for the Federal Reserve

to raise interest rates, leading to a decrease in the money supply. Higher

interest rates equals less borrowing, which constitutes lower investment.Investment

variations which will highly effect new housing starts because of the increased

cost, which may decrease the overall marginal propensity to consume. Lower

rates constitutes the opposite effect which increases investment and the

marginal propensity to consume

With

higher demand for investment mainly for retirement, investors can use these

trends to estimate potential gains and losses in the market. Depending

on the predicted outcome, increases and decreases may be sustainable because

of the constant growth.

The assumption that the M1 money supply is forecast to have an overall decrease in years 2000 through 2001 indicates a decrease in real income, real wealth, and a rising standard of living, for the U.S. throughout the forecast period.

Part 6. Policy Conclusions

The Federal Reserve is responsible for monitoring the supply of the U.S. money supply.Changes in policy can be implemented in three different ways.The control of the supply of U.S. treasury securities, required reserve deposit ratio, and the interest rate level.Due to the minimal change in the quantity of the money supply, government monetary policy changes should not be required for the next two years.M1

is forecast to be approximately 1110.94

billion dollars in the year 2001. This is a 5% increase from 1999. This

value is based on the forecast of GPD to be 9026.946

billion dollars, and Federal Funds Rates to be 5.31.The

Federal Funds Rate has already surpassed that to 5.75 percent, which indicates

a conservative, forecast.

This

forecast assumes the Federal will not raise rates any higher during the

forecast period. Which illustrates an inadequate prediction our forecast.However

the overall forecast seams relatively believable from past economic data.

References

Federal

Reserve Bank of St. Louis, Federal Reserve Economic Database (FRED), http://www.stls.frb.org/fred/

Thomas,

Lloyd B. Money, Banking, and Financial Markets, New York NY: McGraw-Hill

Company, 1996.