KEN HILL Jr.

College of Business

Western Carolina University

Abstract

The Consumer Price Index is projected to increase approximately one half of one percent from December 1999 to December 2001.The estimated annual rate of inflation during this time period is expected to fluctuate between approximately 2 and 4 percent.The forecast is based on the Monetarist Model, using the Quantity of Money Theory of Prices, and assuming a constant Income Velocity.The Consumer Price Index was projected as a linear function of lagged CPI, the M2 measure of the money supply, and the Index of Industrial Production.The forecast indicates considerably slow growth in the CPI and a relatively benign inflation rate. This may persuade firms not to raise prices and may convince the Federal Reserve not to raise interest rates and let the economy continue its fervent rate of growth for the time being.(JEL: E31, E47)

Part 1. Introduction

The rest of this paper is organized as follows: part 2. presents the data used to forecast the CPI, and estimate the annualized rate of inflation; part 3. explains the theoretical basis for the approach adopted in forecasting the CPI; part 4. presents the forecasts of the CPI, and the estimated annual rate of inflation, and the methods used in determining these values; part 5. evaluates the importance of the forecasts for the economy, and part 6. discusses conclusions for economic policy.

Part 2. Data

The forecast horizon is two years into the future.All data used for each variable is readily available, and can be easily accessed on the FRED website http://www.stls.frb.org/fred/index.html.M2 is used as the measure of the money supply, however, alternative measures such as M1, or M3 could be considered as measures of the money supply, and are readily accessible in FRED.

Part 3. The Monetarist Model as a Forecasting Instrument

This model is appropriate since it states that the price level will be determined by the supply of money, and the nations real output.The forecasting equation based on this model uses the CPI as the price level, M2 as the nations money supply, and the Index of Industrial Production as a measure of the nations real output.However, the forecasting equation differs from the Quantity of Money Theory of Prices in that it uses lagged CPI to enhance the determination of the future price level.Two year lagged values are used for all variables in the forecasting equation.The forecasting equation used is

Pt = f(Pt-2, M2t-2, Yt-2).

A major assumption

regarding the forecasting approach is that the Income Velocity will remain

constant.This assumption is appropriate

for a two year forecasting horizon since the Income Velocity is unlikely

to change significantly over such a short period of time.Overall,

a short forecasting horizon of two years is appropriate for the model,

approach, and assumptions utilized in this paper due to other factors that

may affect the price level such as energy shortages.

Part 4. A Short-term Forecast of the Consumer Price Index and the Annualized Rate of Inflation, 2000-2001

Two

year lagged data was used for all variables in generating the least squares

regression estimate. The results of the least squares regression estimate

of the forecasting equation are reported in Table 1.

|

Table 1

Regression Estimate of CPI Forecasting Equation

1: 1990.1-1999.12

|

||

Explanatory variable |

Estimated coefficient |

t-ratio probability level |

Intercept |

|

|

Pt-2 |

|

|

M2t-2 |

|

|

Yt-2 |

|

|

|

|

F (zero slopes) = 7,295.08104 |

Prob F = 3.1E-109 |

There is a very strong linear relationship between the forecast target and the explanatory variables as made evident by a very high R2 of .99581.Furthermore, the validity of the estimated coefficients is substantially supported by their extremely low t-statistic probability levels.It is interesting to note that the coefficient for M2 is negative, which means that an increase in the money supply would result in a decrease in the CPI.At first glance this seems to disprove the legitimacy of the Quantity Theory of Money.However, the negative coefficient for M2 is probably a result of the nations output increasing at a faster rate than the money supply over the past decade.

The forecast results using the ordinary least squares regression along with the estimated annual rates of inflation are reported in Table 2.

|

Forecasts of the Consumer Price Index and Inflation (Annualized

Percentage) 2000.1-2001.12 (Base Year 1982-84, Seasonally Adjusted) |

|||||

|

Month

|

Forecast CPI

|

Forecast Inflation

|

|||

|

2000.1

|

|

|

|||

|

2000.2

|

|

|

|||

|

2000.3

|

|

|

|||

|

2000.4

|

|

|

|||

|

2000.5

|

|

|

|||

|

2000.6

|

|

|

|||

|

2000.7

|

|

|

|||

|

2000.8

|

|

|

|||

|

2000.9

|

|

|

|||

|

2000.10

|

|

|

|||

|

2000.11

|

|

|

|||

|

2000.12

|

|

|

|||

|

2001.1

|

|

|

|||

|

2001.2

|

|

|

|||

|

2001.3

|

|

|

|||

|

2001.4

|

|

|

|||

|

2001.5

|

|

|

|||

|

2001.6

|

|

|

|||

|

2001.7

|

|

|

|||

|

2001.8

|

|

|

|||

|

2001.9

|

|

|

|||

|

2001.10

|

|

|

|||

|

2001.11

|

|

|

|||

|

2001.12

|

|

|

|||

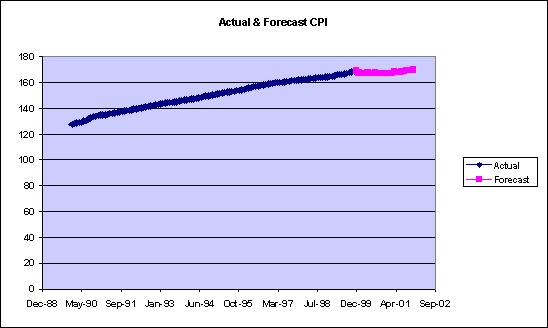

A comparison of actual and forecast CPI from 1990.1 to 2001.12 is shown in Figure 1.

Figure 1

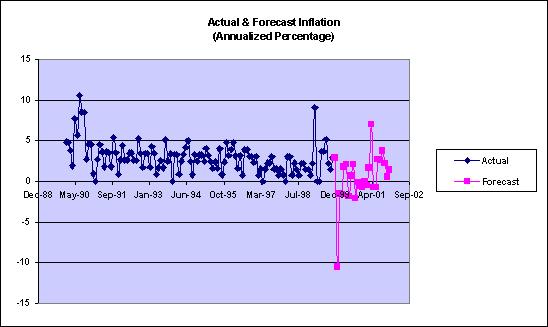

Figure 2 portrays actual and forecast inflation for 1990.1-2001.12.

Figure 2

The forecast indicates a relatively benign increase in the CPI over the next two years.Initially, some negative inflation figures are generated by the forecast, but since negative inflation has not occurred since 1990 the large negative estimates can be disregarded. Overall, the forecast inflation looks to remain fairly stationary ranging from 2.1 up to 3.8 percent, showing no clear upward or downward trend.This outcome would prove to be exceedingly favorable for the nations economy, allowing it to continue to flourish without the threat of inflation.

Part 5. Greenspan Can Rest Easy

The forecast has several favorable implications for the economy, consumers, and the financial markets.Slow growth in the CPI suggests that the economy can continue to grow at its current record setting pace without generating significant upward pressure on prices.This is very good news for the nations economy because it suggests that the current sustained expansion will not be halted by inflation in the near future.This should help economists rest easy for the time being.Stagnant CPI growth is also favorable for consumers.Over the next two years consumers can expect a minimal decrease if not an increase in their real purchasing power.Furthermore, stationary inflation figures would be very beneficial to the financial markets.Since increases in inflation are correlated with increases in interest rates the fixed income markets would welcome low inflation due to the inverse relationship between bond prices and interest rates.The equity markets would also benefit due to the fact that corporate profits would not be significantly impaired by inflation.

Part 6. Policy Conclusions

The CPI is projected to rise by approximately one half of one percent over the next two years.Within the next two years annualized inflation is expected to sustain relatively low levels ranging between 2 to 4 percent.

Assuming that inflation does sustain these considerably low levels businesses can expect a continued robust economy with relatively stable price levels.It will not be necessary for businesses to substantially raise their prices in this low inflationary environment.Businesses may also find equity markets an increasingly attractive source of capital if inflation remains low and the economy continues to prosper.

The Federal Government should continue to act in a fiscally responsible manner, making sure not to over stimulate aggregate demand through excessive tax cuts, which could result in inflationary pressures.The projected forecast should help to ease some of the concerns that the Federal Reserve has regarding inflation.Further interest rate hikes by the Federal Reserve are probably not necessary.The Federal Reserve should consider letting the economy continue to grow at its current rate for the time being.However, longer term, the Federal Reserve still needs to remain vigilant against inflation.